At the recent Angel Capital Association (ACA) Summit in Austin, Texas, the Angel Resource Institute reported on angel group activity in 2011 in the first annual Halo Report. I found some of the results quite interesting. For example:

- The median round of investment by group was about $700,000 but less than $300,000 was invested by the local group leading the deal. Over two-thirds of angel group deals were syndicated with others (mostly other angel groups) who provide the majority of the capital in each round. Furthermore, the median round size was about 40 percent larger in 2011 than in 2010, a really significant increase to me.

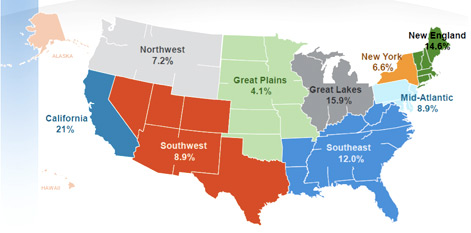

- Only 21 percent of angel deals were done in California, which captures about 40-50 percent of venture capital.

The following graphic demonstrates the broad distribution of angel investment in the US:

Clearly, angel investment is more geographically diverse than venture capital. I was particularly impressed by the number of angel deals done in the Great Lakes and Southeast regions, not generally associated with high entrepreneurial activity.

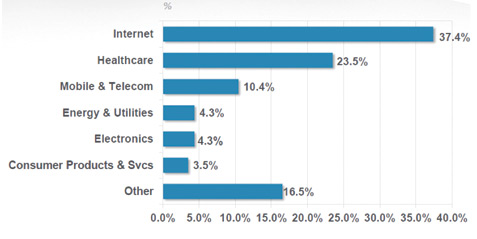

Internet/software deals continue to dominate angel activity with healthcare in a strong second position. Sector investing for angels seems to parallel that of the venture capital community. Of particular interest to me was the “other” category. Angels would appear to be more diverse investors than are VCs because investors tend to invest in the space they know. With an average of 30 or so investors per angel group, we would expect the business sector experience to be broader than that of venture capitalists, which is evidence by the following data: